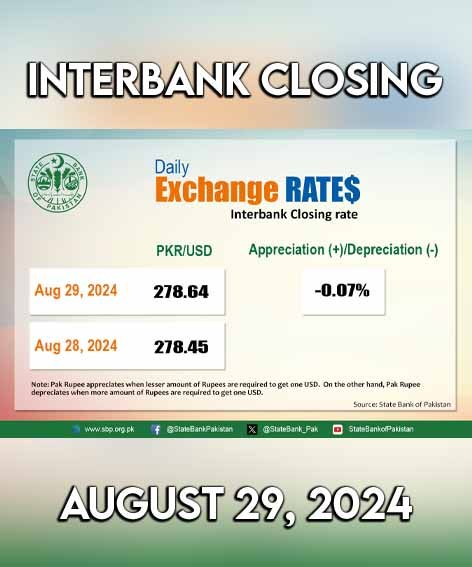

On Thursday, the Pakistani rupee (PKR) saw a slight depreciation of 19.23 paisa, or 0.07 per cent, against the US dollar (USD) in the interbank market.

The rupee settled at PKR 278.64 per USD, compared to the previous closing rate of PKR 278.45. Throughout the trading session, the rupee reached an intraday high bid of PKR 278.80 and an intraday low ask of PKR 278.70.

In the open market, exchange companies quoted the USD at PKR 279.13 for buying and PKR 280 for selling.

Here’s how Pakistani currency performed against other major currencies:

Currency

Change

Previous rate

Thursday’s rate

Swiss Franc

+50.26 paisa

330.25

330.75

British Pound

-38.65 paisa

368.46

368.07

Euro

+1.12 rupee

310.72

309.60

Chinese Yuan

+13.78 paisa

39.06

39.20

Japanese Yen

+0.01 paisa

1.9261

1.926

Saudi Riyal

+4.93 paisa

74.21

74.26

UAE Dirham

+5.24 paisa

75.86

75.81

PKR exchange rates for Thursday

In comparison to other major currencies, the Swiss franc gained 50.26 paisa, closing at PKR 330.75, up from PKR 330.25 in the previous session. Conversely, the British pound depreciated by 38.65 paisa, settling at PKR 368.07, compared to PKR 368.46 from the day before.

The PKR also strengthened against the Euro, gaining 1.12 rupees to close at PKR 309.60, up from PKR 310.72. The Chinese yuan saw an increase of 13.78 paisa, closing at PKR 39.20 compared to PKR 39.06 previously.

Against the Japanese yen, the PKR gained 0.01 paisa, ending at PKR 1.926, compared to PKR 1.9261 a day earlier. The Saudi riyal closed at PKR 74.26, reflecting a gain of 4.93 paisa from PKR 74.21 the previous day. The UAE dirham appreciated by 5.24 paisa, closing at PKR 75.81 compared to PKR 75.86.

In recent months, the PKR has largely fluctuated between PKR 277 and PKR 279 as traders await approval from the International Monetary Fund’s (IMF) Executive Board for a new $7 billion Extended Fund Facility. In a positive development,

Moody’s Ratings upgraded Pakistan’s local and foreign currency issuer and senior unsecured debt ratings from Caa3 to Caa2. Moody’s also anticipates IMF approval for Pakistan’s Extended Fund Facility in the coming weeks.

Globally, the US dollar stabilised on Thursday, recovering some of its previous losses. Traders are now looking forward to a key US inflation report at the end of the week, which may provide further insights into the future direction of interest rates.

So far in the current financial year, the PKR has depreciated against the dollar by 30.11 paisa, or 0.11 per cent. However, for the calendar year, the PKR has appreciated by 3.22 rupees, or 1.16 per cent.

Foreign exchange reserves held by the State Bank of Pakistan (SBP) saw a rise of $112 million over the past week, bringing the total to $9.4 billion as of August 23, according to data released on Thursday.

“During the week ending on August 23, 2024, SBP reserves increased by $112 million, reaching $9.4 billion,” the bank stated in its report. This follows a smaller increase of $19 million the previous week.

In total, the country’s liquid foreign reserves reached $14.77 billion, with commercial banks holding $5.37 billion of this amount. The central bank did not provide any specific reason for the increase in its reserves.

The rise in reserves comes as Pakistan seeks to raise up to $4 billion from Middle Eastern commercial banks by the next fiscal year (FY26). This effort is part of a broader strategy to address the country’s external financing needs, as explained by SBP Governor Jameel Ahmad in a recent interview.

Ahmad also mentioned that Pakistan is in the final stages of securing an additional $2 billion in external funding, which is crucial for obtaining the International Monetary Fund (IMF) approval for a $7 billion bailout programme.

In related financial news, the international price of gold rose to $2,516 per ounce on Thursday, marking an increase of $4 during the day, according to the All Pakistan Gems and Jewellery Traders and Exporters Association (APGJSA). Silver prices, however, remained steady at Rs2,950 per tola.

Gold prices in Pakistan experienced a notable decline on Thursday, reversing the momentum of consecutive record highs achieved in the previous sessions.

This drop in local gold rates occurred despite an uptick in international prices, reflecting a divergence between domestic and global trends.

In the local market, the price of gold per tola fell by Rs2,200, bringing it down to Rs261,500. Similarly, the price of 10-gram gold witnessed a decrease of Rs1,886, settling at Rs224,194, as per the rates provided by the All-Pakistan Gems and Jewellers Sarafa Association (APGJSA).

This decline comes after a steady increase that saw gold prices reach Rs263,700 per tola on Saturday, following a rise of Rs1,700.

Contrary to the local market trend, the international gold price edged up on Thursday. According to APGJSA, the global rate for gold was reported at $2,516 per ounce, including a premium of $20, marking an increase of $4 during the day.

Despite this rise in international prices, the local market’s reaction suggests other factors at play in determining gold prices in Pakistan.

Meanwhile, silver prices in the local market remained stable, with no change reported. The rate for silver stood firm at Rs2,950 per tola, reflecting a steady demand and supply situation.

This fluctuation in gold prices highlights the complexities of the market, influenced by both domestic and international factors, making it a subject of keen interest for investors and consumers alike.

Moody’s Investors Service has upgraded Pakistan’s long-term issuer rating from “Caa3” to “Caa2” with a stable outlook, reflecting a moderate improvement in the country’s macroeconomic conditions and external financial position.

This decision follows a similar move by Fitch Ratings in July, which upgraded Pakistan’s credit rating from “CCC” to “CCC+.”

Moody’s stated that the upgrade is a result of reduced default risks, which are now more consistent with a Caa2 rating.

This improvement is partly due to greater certainty in Pakistan’s external financing, bolstered by the sovereign’s staff-level agreement with the International Monetary Fund (IMF) on 12 July 2024, for a 37-month Extended Fund Facility (EFF) worth $7 billion. The IMF Board is expected to approve the EFF in the coming weeks.

Pakistan’s foreign exchange reserves have nearly doubled since June 2023, although they remain below the levels required to meet its external financing needs. The country continues to rely on timely support from official partners to fully meet its external debt obligations.

Despite the upgrade, Pakistan’s Caa2 rating still reflects very weak debt affordability, which poses a significant risk to debt sustainability. Moody’s expects interest payments to consume about half of the government’s revenue over the next two to three years. The rating also takes into account the country’s weak governance and high political uncertainty.

The stable outlook indicates a balance of risks, with potential for further improvement if the government can reduce its liquidity and external vulnerability risks and achieve better fiscal outcomes, supported by the IMF programme.

Sustained implementation of reforms, particularly those aimed at increasing government revenue, could enhance debt affordability. Timely completion of IMF reviews would enable Pakistan to secure continued financing from official partners, essential for meeting external debt obligations and rebuilding foreign exchange reserves.

The upgrade to Caa2 from Caa3 also applies to the backed foreign currency senior unsecured ratings for The Pakistan Global Sukuk Programme Co Ltd, which Moody’s views as direct obligations of the Government of Pakistan. The outlook for The Pakistan Global Sukuk Programme Co Ltd is positive.

Additionally, Moody’s has raised Pakistan’s local and foreign currency country ceilings to B3 and Caa2 from B3 and Caa1, respectively.

The two-notch gap between the local currency ceiling and the sovereign rating is due to the government’s significant role in the economy, weak institutions, and high political and external vulnerability risks.

The two-notch gap between the foreign currency ceiling and the local currency ceiling reflects limited capital account convertibility and relatively weak policy effectiveness.

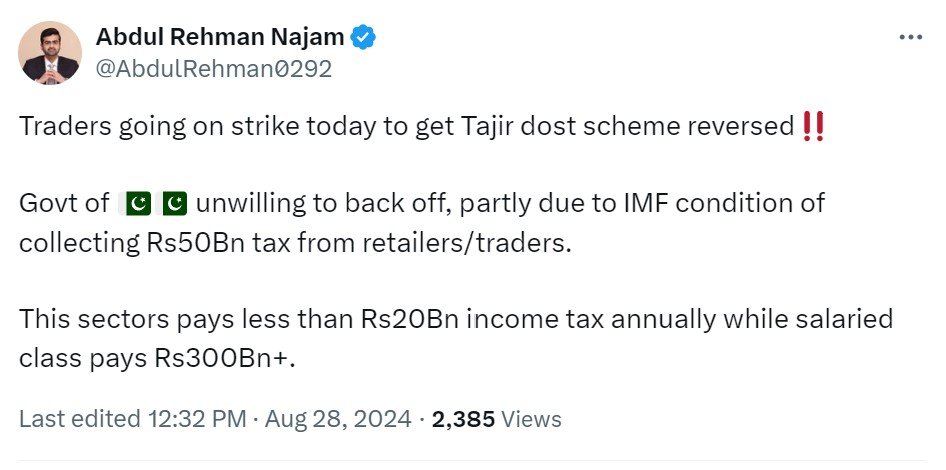

Traders across the country are observing a nationwide strike on August 28 to protest against the government’s tax reforms.

Many political parties, including Jamiat Ulema-e-Islam Fazl (JUI-F), Pakistan Tehreek-e-Insaf (PTI), Jamaat-e-Islami (JI), and the Awami National Party (ANP), are supporting the traders’ strike.

Traders’ representatives visited the Federal Board of Revenue (FBR) headquarters to express their reservations about the Tajir Dost Scheme, the government’s initiative to bring retailers and traders into the tax net.

FBR Chairman Rashid Mahmood told Dawn that the FBR will not withdraw the Tajir Dost Scheme; however, it was willing to resolve the “legitimate issues” the traders may be facing.

According to the Chairman, the retail sector contributes around 20 percent to the GDP, yet it remains largely untaxed.

Social media had no patience for the traders.

One social media user posted on X, formerly Twitter, that the retail sector pays less than Rs20 billion income tax annually while the salaried class pays more than Rs300 billion annually.

Similarly, another netizen took to X to condemn the political parties supporting the traders’ strike because they will be supporting “one of biggest chor sector of retail and wholesale in Pakistan.”

Pakistan plans to raise up to $4 billion from Middle Eastern commercial banks by the fiscal year 2026, according to the Governor of the State Bank of Pakistan (SBP), Jameel Ahmad.

In his first interview since assuming office in 2022, Ahmad revealed that Pakistan is also in the final stages of securing an additional $2 billion in external financing, which is essential for the approval of the $7 billion bailout programme from the International Monetary Fund (IMF).

The IMF and Pakistan reached a preliminary agreement on the loan in July. However, the agreement still needs approval from the IMF’s executive board and confirmation of financing assurances from Pakistan’s development and bilateral partners.

Ahmad expressed confidence that Pakistan’s financing needs will be met smoothly in the next fiscal year and in the medium term. Historically, Pakistan has depended on long-time allies like China, Saudi Arabia, and the UAE to extend loans rather than demand immediate repayment. Ahmad expects similar support for the next three years, giving the government more time to stabilise its finances.

He also mentioned that Pakistan’s financing needs might be lower than the 5.5 per cent of GDP projected by the IMF. This is because the country’s external financing requirements have been declining, and the IMF’s projections were based on a higher current account deficit than what has materialised.

Regarding monetary policy, Ahmad noted that recent interest rate cuts have successfully reduced inflation, which stood at 11.1 per cent in July, down from over 30 per cent in 2023. He emphasized that future interest rate decisions would be based on economic developments. Pakistan’s central bank had reduced interest rates from a record high of 22 per cent to 19.5 per cent and will review its monetary policy again on September 12.

Ahmad, reflecting on his first year as governor, described it as challenging but expressed optimism that the situation has improved, with a focus now on growth, digitalisation, and financial inclusion.

The Pakistani rupee (PKR) appreciated by 9.62 paisa, or 0.03 per cent, against the US dollar during Tuesday’s interbank session, closing at PKR 278.32 per USD, compared to the previous rate of PKR 278.42.

Throughout the session, the currency fluctuated, with an intraday high of PKR 278.40 and a low of PKR 278.20. In the open market, exchange companies quoted the dollar at PKR 279.12 for buying and PKR 280.00 for selling.

Currency

Change (Paisa)

Closing rate (PKR)

Previous rate (PKR)

Euro

+37.19

310.87

311.24

British Pound

+23.5

367.59

367.36

Swiss Franc

-46.25

328.34

328.81

Japanese Yen

+1.46

1.9197

1.9343

Chinese Yuan

-6.78

39.03

39.10

Saudi Riyal

-2.56

74.18

74.20

UAE Dirham

-2.62

75.80

75.78

Exchange rates

In relation to other major currencies, the PKR gained 37.19 paisa against the Euro, closing at PKR 310.87, up from the previous value of PKR 311.24.

The Saudi Riyal closed at PKR 74.18, down by 2.56 paisa from its previous value of PKR 74.20. Similarly, the U.A.E Dirham decreased by 2.62 paisa, closing at PKR 75.80 from PKR 75.78 a day earlier.

The British Pound became slightly more expensive, rising by 23.5 paisa to close at PKR 367.59, compared to the previous close of PKR 367.36. The Swiss Franc saw a loss of 46.25 paisa, closing at PKR 328.34, down from PKR 328.81.

Against the Japanese Yen, the PKR gained 1.46 paisa, closing at PKR 1.9197, compared to PKR 1.9343 the previous day. The Chinese Yuan lost 6.78 paisa, closing at PKR 39.03, down from PKR 39.10 in the previous session.

During the current financial year, the PKR has appreciated by 2.01 paisa, or 0.01 per cent, against the US dollar. Meanwhile, in the current calendar year, the PKR has strengthened by PKR 3.54, or 1.27 per cent.

Prospective buyers of Pakistan International Airlines (PIA) have expressed reluctance to retain the airline’s employees. On Monday, the National Assembly panel recommended that the government order the buyer to retain all its employees for five years.

Express Tribune reported that some bidders also indicated that all employee liabilities up to the bid date should be the government’s headache.

Muttahida Quami Movement (MQM) leader Muhammad Farooq Sattar, who chaired the standing committee, urged that PIA’s employees be retained for at least five years and that the workers’ union be involved.

The draft Share, Purchase and Subscription Agreement currently proposes that existing employees, regardless of their position, cannot be terminated, laid off, retrenched, or forced to resign for three years from the completion date, except in misconduct cases. However, Secretary of the Privatisation Ministry Jawad Paul noted that this is still being determined.

He also stated that PIA has incurred Rs499 billion in losses since 2015, with cumulative losses reaching Rs842 billion.

The government is required to conduct a special audit of PIA’s accounts by June 30th, a requirement before its privatisation.

The Lahore district administration has intensified its efforts against overpricing, resulting in significant fines and the arrest of two individuals.

Under the directives of District Commissioner Lahore Syed Musa Raza, assistant commissioners carried out surprise inspections at over 1,700 locations. These inspections led to the registration of eight cases and the imposition of fines totaling Rs1.1 million for 187 violations.

The crackdown primarily targeted shopkeepers who were selling essential food items at prices higher than the government-mandated rates. This issue has been a growing concern in Pakistan, where overcharging by vendors exacerbates the financial strain on consumers already struggling with high inflation. The situation is particularly dire for low-income earners, who find it increasingly difficult to afford basic necessities.

Assistant Commissioner Model Town, Sahibzada Muhammad Yousaf, conducted price inspections at various tandoors and shops, imposing fines of Rs25,000 for violations. Similarly, Assistant Commissioner Shalimar, Anam Fatima, sealed a tandoor during inspections in Tajpura and Harbanspura.

In the Band Road Saggian area, Assistant Commissioner City, Rai Babar, inspected several shops and tandoors, issuing warnings and fines to multiple owners. Assistant Commissioner Raiwind, Zainab Tahir, carried out inspections at Raiwind Mandi and Rehri Bazaar Bhatta Chowk, fining two shopkeepers on the spot following consumer complaints.

Authorities have mandated that all stalls and shops prominently display government-issued rate lists. Strict action will be taken against those who fail to comply. Following directives from the Chief Minister of Punjab, the administration has made it clear that there will be zero tolerance for overpricing.

In a related development, the price of table eggs in Lahore has surpassed Rs300 per dozen, reaching Rs301. Despite no significant change in demand or production costs, egg prices have steadily increased in recent weeks. Conversely, the price of broiler chicken meat has decreased by Rs18 per kilogramme, settling at Rs577 per kilogramme after a brief downward trend.

Weekly inflation eases slightly, but challenges remain

Short-term inflation in Pakistan eased slightly by 0.10 per cent to a 27-month low of 16.69 per cent for the week ending August 22, 2024, compared to the same period last year. According to data from the Pakistan Bureau of Statistics (PBS), the decline was primarily driven by lower prices of tomatoes, which fell by 21.96 per cent, and wheat flour, which dropped by 2.77 per cent.

However, the prices of several essential items, including eggs (up 6.10 per cent), pulse gramme (up 6.05 per cent), and potatoes (up 2.41 per cent), continued to rise. The PBS data showed that out of 51 tracked items, 21 experienced price increases, nine saw decreases, and 21 remained stable during the week.

On a year-on-year basis, inflation was up by 16.69 per cent, with significant increases in the prices of gas charges (up 570 per cent), onions (up 79.51 per cent), and pulse gramme (up 51.34 per cent). Despite some declines in the prices of wheat flour, electricity charges, and certain cooking oils, the overall inflationary trend remains a significant concern for consumers.

As the government continues its crackdown on overpricing, the broader challenge of managing inflation and ensuring affordability for essential goods remains critical for the well-being of Pakistan’s population.

Gold prices in Pakistan soared to unprecedented levels on Saturday, reflecting a continued upward trend driven by rising international rates.

In the local market, the price of gold per tola (approximately 11.66 grammes) surged by Rs1,700, reaching a new record high of Rs263,700.

This significant increase underscores the precious metal’s enduring appeal as a safe haven amid global economic uncertainties.

The price of 10-gramme gold, a popular metric among consumers, also saw a substantial rise, climbing by Rs1,457 to settle at Rs226,080, according to the latest data released by the All-Pakistan Gems and Jewellers Sarafa Association (APGJSA).

These sharp increases come on the back of a minor gain of Rs200 recorded on Friday, when the price per tola stood at Rs262,000.

The surge in domestic gold prices is largely attributed to a parallel increase in international rates. On Saturday, the international price of gold rose by $20 (PKR 5,526), bringing it to $2,512 (PKR 694,169) per ounce, inclusive of a premium of $20.

The upward trajectory of gold prices on the global stage is driven by a combination of factors, including persistent inflation concerns, geopolitical tensions, and fluctuating currency values.

As investors seek refuge in the stability of gold, demand for the precious metal continues to push prices higher, with ripple effects felt across markets worldwide, including Pakistan.

Silver rate in Pakistan

While gold prices surged, silver remained stable in the local market. The price of silver per tola held firm at Rs2,950, showing no change from the previous sessions.

Despite its status as a precious metal, silver has not experienced the same level of price volatility as gold, largely due to differing market dynamics and industrial demand.

Week in review: Gold’s record-breaking streak

Day

Price per tola (Rs)

Price change (Rs)

Details

Monday

260,000

-200

Slight decrease after a record high in the previous session.

Tuesday

260,700

+700

New record high reflecting an uptick in international rates.

Wednesday

261,000

+300

Continued upward trend, marking the third record in a month.

Thursday

261,800

+800

All-time high, still Rs3,000 below market value.

Friday

262,000

+200

Highest price ever recorded in Pakistan until Saturday.

Saturday

263,700

+1,700

New record high, significant rise.

Gold price history (trade week ending: August 24)

This week has been particularly eventful for gold prices in Pakistan, marked by consistent daily increases that have culminated in Saturday’s record-breaking levels.

Monday: The week began with a slight dip in gold prices, following a record high in the previous session. The price of 24-karat gold fell by Rs200, settling at Rs260,000 per tola. Interestingly, even with this decrease, the price remained Rs4,000 below its actual market value, indicating underlying bullish sentiment.

Tuesday: Gold prices rebounded sharply on Tuesday, reaching a new record high. The price per tola increased by Rs700, bringing it to Rs260,700. This surge mirrored an uptick in international rates, reinforcing the connection between local and global market trends.

Wednesday: The upward momentum continued on Wednesday, with gold prices in Pakistan reaching another new record. The price of 24-karat gold per tola rose by Rs300, setting a new high at Rs261,000.

This marked the third record-breaking price level within the month, highlighting the sustained demand for gold.

Thursday: On Thursday, gold prices soared to an all-time high of Rs261,800 per tola, following an increase of Rs800. Despite this, the price was still Rs3,000 below its estimated market value, suggesting that the metal’s true worth is yet to be fully reflected in the market.

Friday: The upward trajectory of gold prices continued for the fourth consecutive day on Friday, with the price per tola reaching Rs262,000 after a modest increase of Rs200. This marked the highest price ever recorded for gold in Pakistan, setting the stage for Saturday’s further escalation.

Implications for consumers and investors

The relentless rise in gold prices has significant implications for both consumers and investors in Pakistan. For those who have invested in gold, the ongoing price surge represents a substantial return on investment, particularly for those who purchased the metal when prices were lower.

However, for consumers looking to buy gold for personal use, such as jewellery or gifts, the soaring prices are increasingly prohibitive. The current levels have made gold almost out of reach for many, particularly in a country where gold is deeply embedded in cultural traditions and ceremonies.

This price hike is a double-edged sword—beneficial for investors but challenging for those with other intentions. The persistent rise in gold prices may push consumers to explore alternative options, while investors continue to benefit from the metal’s role as a hedge against economic instability.

Gold’s record-breaking streak in Pakistan, fuelled by global market dynamics, highlights the precious metal’s enduring value and the challenges it poses for local consumers.

As the international market remains volatile, the question remains whether gold prices will continue to rise or if a correction is on the horizon. For now, the allure of gold remains as strong as ever, both as an investment and a symbol of wealth.