The Pakistan Stock Exchange (PSX) had a rough start on Friday, with the KSE-100 Index dropping by 0.79 per cent in early trading.

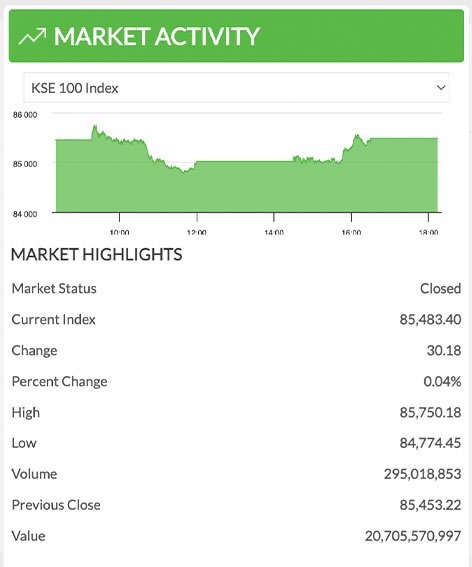

By the end of the day, the index managed to recover marginally and closing almost flat at 85,483.40 points. The gain PSX witnessed was just 30.18 points, or 0.04 per cent.

During trading hours, the index swung up and down within a range of 975 points. KSE-100 reached a high of 85,750 points and dipped to a low of 84,774 points. A total of 295 million shares were traded within the PSX.

| Top gainers | Change (%) | Top decliners | Change (%) |

| ATLH | +10.00% | KOSM | -11.84% |

| PTC | +8.13% | HUBC | -5.17% |

| PIOC | +7.50% | YOUW | -4.75% |

| PSO | +5.16% | ABL | -3.39% |

| ATRL | +3.88% | LUCK | -3.28% |

Out of the 100 listed companies, 46 witnessed gains, 50 ended red, and 4 stayed same. The top gainers of Friday were companies including ATLH (+10.00 per cent), PTC (+8.13 per cent), PIOC (+7.50 per cent), PSO (+5.16 per cent), and ATRL (+3.88 per cent).

On the losing side, the biggest decliners were KOSM (-11.84 per cent), HUBC (-5.17 per cent), YOUW (-4.75 per cent), ABL (-3.39 per cent), and LUCK (-3.28 per cent).

In terms of influencing overall index, PSO had the biggest positive impact, adding 68.72 points to the index, followed by FFC, EFERT, PIOC, and lastly UBL.

Secondly, HUBC dragged the index down the most, bringing it down by 181.94 points, with LUCK, HBL, TRG, and SRVI also contributing to the drop.

Overall, 560.74 million shares were traded across the stock market, up from 503.75 million on Thursday The total value of shares traded was recoeded Rs26.12 billion, which was Rs1.79 billion less than the last session.