Federal Minister for Finance and Revenue Ishaq Dar has categorically denied rumours suggesting that the government is considering “access to foreign exchange held with commercial banks.”

“It is categorically denied and clarified that there is no such move under consideration of the government,” said Dar, in a series of tweets.

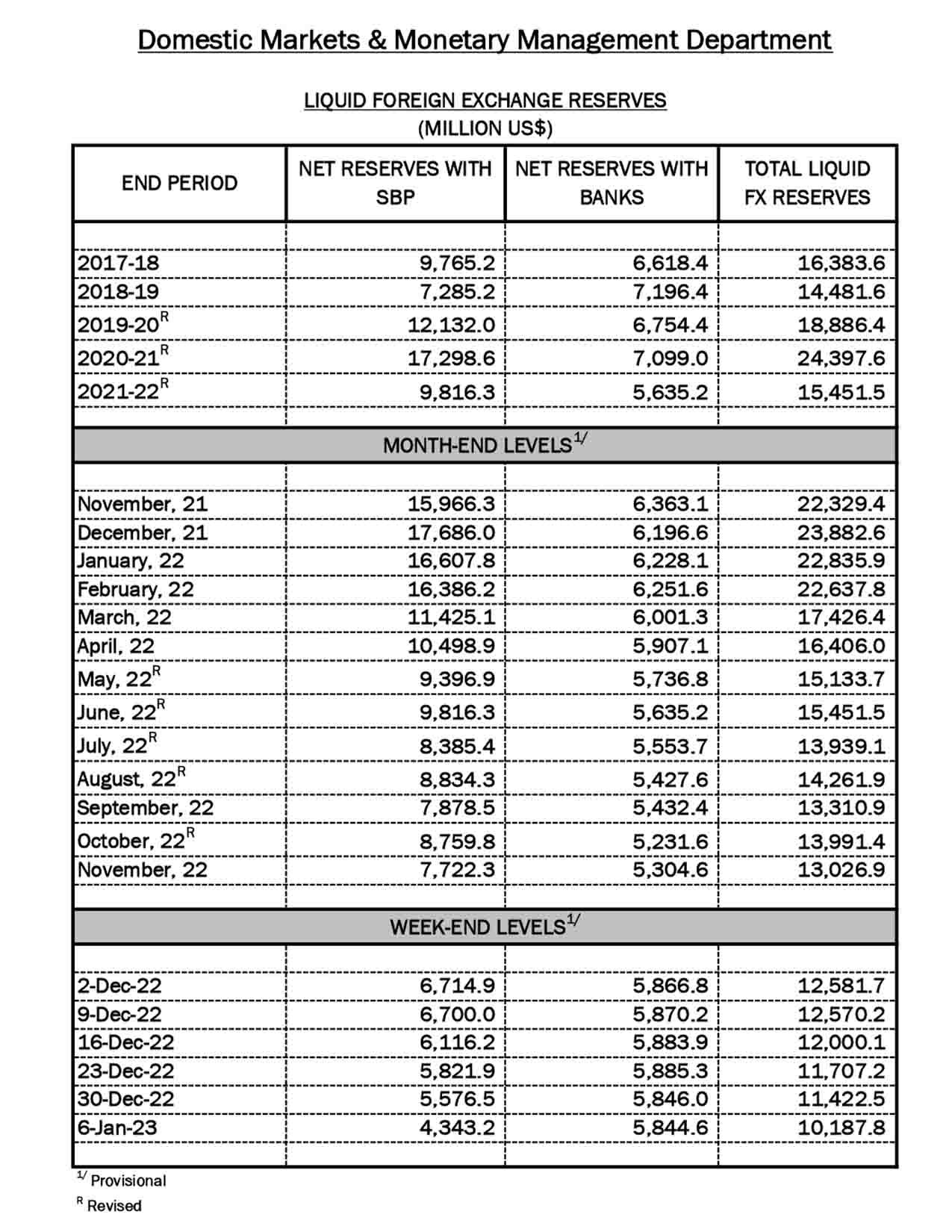

The statement come days after the finance minister said that the country’s foreign exchange reserves stand at $10 billion, a much higher amount than the SBP’s $5.6 billion reserves as of December 30, 2022, since “dollars held by commercial banks also belonged to the country.”

This comment gave rise to fears that the government may confiscate dollars from private banks as had been done in 1998 when Dar was the finance minister.

However, Dar said that his comment was “greatly misconstrued” and nothing like this would happen.

Dar explained at a press conference with Prime Minister Shehbaz Sharif and other federal cabinet members that before 1999, all foreign currency was deposited with the State Bank of Pakistan (SBP), and private banks were not permitted to hold any foreign currency.

“In February 1999, when I was the finance minister, we devised a system whereby a substantial amount [of dollars] remain with [private] banks. It was on June 30, 1999 that reserves were broken down into three columns — those with the SBP, commercial banks and total.

“Whenever Pakistan’s reserves are quoted anywhere in the world — a survey or a document — the [total figure] is quoted and then a breakdown is given. I gave a breakdown too,” he added.

The minister claimed that certain people were to blame for the country’s dire circumstances, which caused it to drop from the 24th to the 47th largest economy in 2016.

“Even now, they cannot tolerate any good development. They gave such a twist [to my statement],” he said, adding that while the federal cabinet was busy working for Pakistan under PM Shehbaz’s guidance, such people were spreading rumours that the government would take dollars from commercial banks.

“Nothing of that sort will happen. Everything is all worked out … and in order. Nothing to worry about,” he assured, urging those “spreading the rumours” to play a positive national role.

Dar also tweeted about the reserves later, saying national foreign exchange reserves always include forex held with SBP and commercial banks.

Furthermore, Dar tweeted about the reserves and stated that SBP and commercial bank holdings are usually included in the nation’s foreign exchange reserves.

“Recently I quoted the forex reserves figure based on this principle. Some vested elements who ruined this country’s economy in the past, gave it a deliberate twist and started a campaign as if govt was considering access to foreign exchange held with commercial banks which indeed is the property of the citizens.

“It is categorically denied and clarified that there is no such move under consideration of the government,” he emphasised.

The finance minister once again claimed that Pakistan’s foreign exchange reserves would increase soon.

As of December 30, 2022, Pakistan’s foreign exchange reserves had decreased to $5.6 billion, an eight-year low. This is equivalent to imports for three weeks.

The swift decrease has made it impossible for the government to repay its international debts without taking out new loans from allies.

Govt to comply with IMF conditions without burdening common man

The International Monetary Fund (IMF) programme’s ninth review, which would release $1.18 billion, has been postponed for months due to the government’s refusal to comply with some conditions imposed by the international lender.

In today’s press conference, Dar acknowledged the delay and claimed that it was due to revenue collection. The Federal Board of Revenue (FBR) missed its goal in December, the finance minister said, and the super tax that the administration enacted in June of last year had been declared unlawful by a high court.

Dar said that his team informed the IMF that Pakistan could recover the amount easily after the Supreme Court takes a decision on the super tax.

“We are not changing the fiscal budget target and we will achieve it,” he claimed.

Dar said that the IMF suggested that the government implement fiscal measures and eliminate some subsidies. “We have identified some budgetary measures, but the average person won’t be overburdened.”

He asserted that the measures would be very specific and classified.