Pakistan is escalating efforts in order to revive the stalled loan from International Monetary Fund (IMF) programme, as the prerequisites are steadily being completed.

The revival of the bailout will provide much-needed relief in order to keep Pakistan’s economy afloat and avoid default as Pakistani currency has plummeted 9 per cent in the last month, recording the poorest performance among Asian currencies.

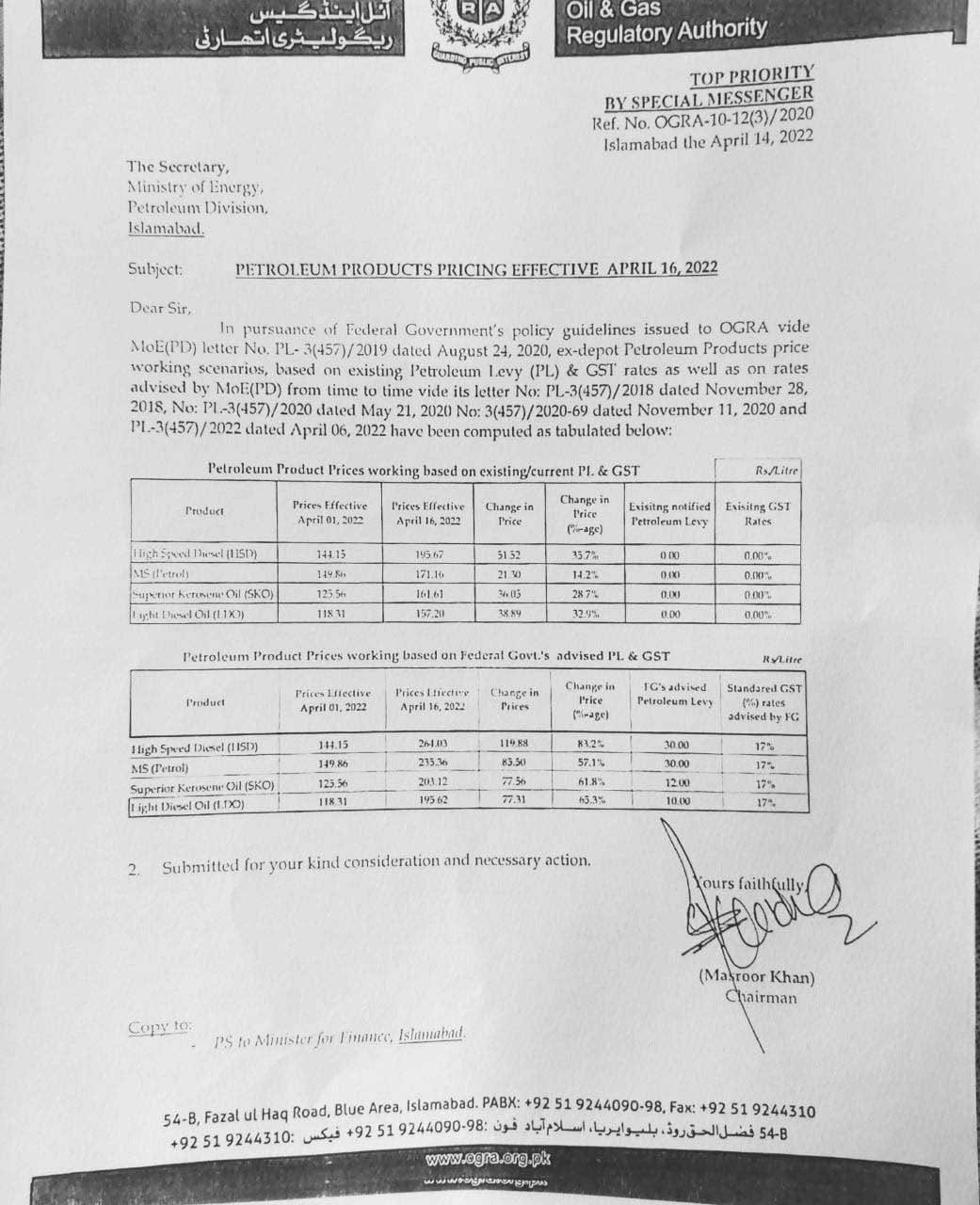

According to Geo, the key policy rate was recently raised by 150 basis points to 13.75 per cent, while the price of fuel has now risen by Rs60 a litre in less than a month and is being sold at from Rs209 to Rs212 (depending on the area).

In an interview with a private channel, the finance minister discussed the government’s decision to raise petroleum product pricing, saying that despite the difficult decision, the government is still losing money on gasoline and diesel.

These moves are highly affecting the masses, but they are essential as the IMF programme is crucial to fix the country’s economy. Also, petroleum prices are projected to continue to rise along with power tariff.

Increase in income tax

An increase in income tax is a major policy recommendation from the international lender in the approaching budget for the fiscal year 2022-23.

All suggestions are expected to enhance Pakistan’s tax income.

The IMF issued the following rules for Personal Income Tax (PIT) in its February conditions:

- Lower the number of tax bands.

- Cut tax credits and allowances (excluding disabled and old persons, as well as Zakat receipts).

- Implement special tax processes for very small taxpayers.

- Increase the number of people who pay taxes. As the change maintains the present PIT threshold, low-income households will be safeguarded (almost three times income per capita).

If these policy recommendations for the forthcoming budget are enacted, the tax system will be simplified and the income tax regime will be more progressive.

These recommendations are anticipated to increase the country’s tax revenue. It will also make the system more progressive, as people with higher incomes will be required to pay more.

Salaried class

The burden on the salaried class, which is already heavily under pressure, may be increased. It will make working less appealing because a large portion of the wage will be devoted to direct personal income tax.

The IMF proposed taxing the upper-middle class and wealthy individuals with monthly incomes ranging from Rs104,000 to Rs1 million at a uniform rate of 30 per cent.

The idea demonstrates inequality in taxation, and if approved, it might leave the majority of salaried workers worse off in the face of double-digit inflation.

On the other hand, Federal Minister for Finance and Revenues Miftah Ismail categorically stated last month that the government would not add to the burden on the salaried class and pensioners in the coming budget.

According to sources, the maximum rate of 30 to 35 per cent for salaried and business class individuals earning Rs20 million per year could be increased.

Special tax proposal for small taxpayers

Imposing a tax on small taxpayers can overcome the long-term structural problems and correct internal and external imbalances. Our tax-to-GDP ratio has remained below 11 per cent, which is lower than regional standards.

Two-thirds of our overall taxation is made up of indirect taxation. This level of indirect taxation is not only excessive, but it also makes the system less progressive.

Currently, a labourer pays the same amount of GST as the country’s richest man.

Agriculturalists and real estate barons are the most important import consumers. As a result, the lack of taxation in agricultural and real estate contributes to the underlying imbalances in the external sector.

Low-income households

Low-income households are expected to be protected from policy interventions after the government publishes the upcoming budget, as the Personal Income Tax (PIT) threshold of three times per capita income would stay in place.

Genuine taxpayers can also decrease their tax payments by clever investments under the Income Tax Ordinance 2001, taking into account all of the foregoing.

In the fiscal year 2022-23, policymakers must aim to increase the tax net and the tax-to-GDP ratio as there is no chance for the country to progress without it.

Pakistan must pay $21 billion in foreign debt payments by next year, according to the Finance Minister, while the current account deficit is $10-12 billion.

He said, “We will also try to tilt away from the wealthy elite towards to low incoming masses, I will impose more taxes on the wealthy, but no taxes will be levied on the salaried class”.

The wealthy and capable must prepare to pay their fair share of taxes, or the country will soon be back on the IMF’s doorstep.