On Tuesday, the Pakistani currency experienced a significant decline, reaching a new record low of Rs308 against the US dollar in the open market. This marked a 1 per cent decrease, or Rs3, from the previous day’s closing rate, as reported by the Exchange Companies Association of Pakistan.

Consequently, the disparity between the exchange rates in the open market and the inter-bank market widened considerably, reaching a historic high of Rs21 to a dollar. Just a couple of months ago, this difference was in the range of Rs1-3.

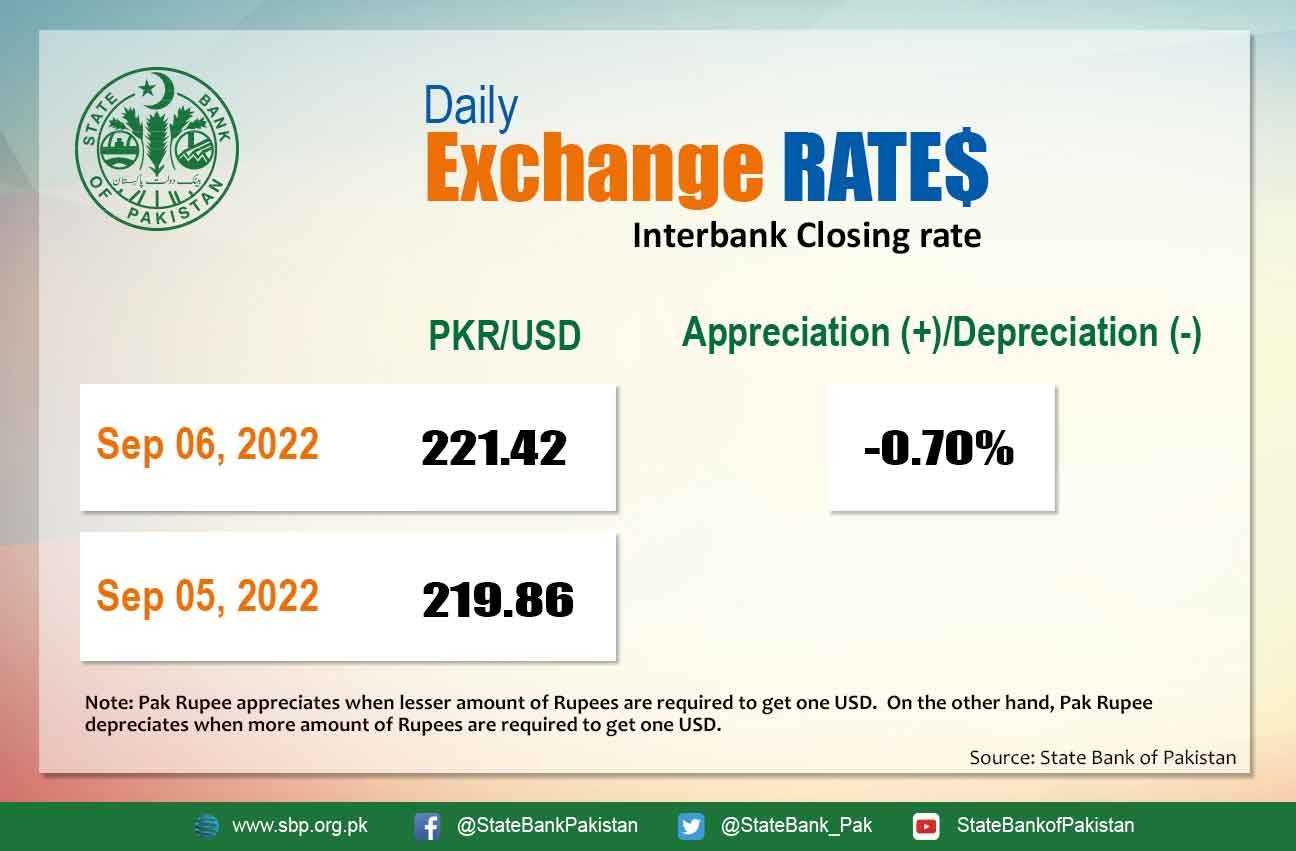

In inter-bank transactions, the central bank stated that the rupee continued its downward trend for the fifth consecutive working day, dropping by 0.21 per cent, or Rs0.59, to a 12-day low at Rs287.15 against the US dollar.

There has been speculation in the market that the rupee is facing mounting pressure due to the expanding gap between the demand and supply of the US dollar in the currency market.

In the meantime, Pakistan’s foreign exchange reserves have been consistently depleting and have now reached a critically low level of $4.3 billion. This is concerning because the country requires a comparatively large amount of foreign currency to cover import expenses and repay foreign debt.

By the end of June 2023, Pakistan has to repay $3.7 billion in foreign debt. Additionally, it needs another $3.7 billion each month to ensure smooth importation of essential goods.

Currency dealers in the open market have revealed that commercial banks are purchasing dollars in the informal market (kerb market) to settle international payments made through their clients’ credit cards. Furthermore, individuals are acquiring Saudi riyals and US dollars to cover expenses during the Hajj and Umrah pilgrimages.

Experts strongly emphasize that the government must persuade the International Monetary Fund (IMF) to resume its $6.7 billion loan programme. Additionally, they urge friendly countries to provide fresh financing, which will help mitigate the risk of defaulting on external debt obligations.

The resumption of the IMF programme will not only assist Pakistan in averting an imminent default but will also enable the country to attract financing from other global lenders and friendly nations. This new financing will bolster the foreign exchange reserves and aid in the reopening of the partially closed economy.