The federal budget for 2022-23 has been revealed with a total outlay of Rs9,502 billion. It includes measures for sustainable economic growth, industrial and agricultural development, and aid for the poor ones.

Finance Minister, Miftah Ismail began his address by claiming that the PTI administration had left Pakistan’s economy in shambles and harmed investor confidence by often switching finance ministers and monetary policies.

He slammed former Prime Minister Imran Khan, claiming that he never cared about the poor, claiming that “keeping an eye on potato and tomato prices is not a PM’s duty”.

He claims that the governing party took control of the country despite the fact that it will have to make difficult decisions to save the economy, which will affect their individual parties’ appeal, but they chose to put the country’s interests ahead of their own.

Relief for working class and the poor

He claimed that the budget is geared at providing greater relief to the working class and the poor, as opposed to the wealthy, because the working class prefers to buy local products over foreign ones, boosting the economy.

Budget 2022-23, according to Miftah Ismail, will concentrate on offering facilities to farmers planting crops that supply cooking oil, such as corn and sunflower, so that the country does not need to import palm oil, which is at an all-time high in the worldwide market.

Slashing furniture, stationary expenses in govt offices

Considering the current economic downturn, the administration has decided to restrict operational expenditures to the absolute minimum, and that new furniture and stationary for government offices will be completely prohibited. Other than obligatory diplomatic visits, all government-sponsored foreign trips will be prohibited.

Education

The government has set aside Rs65 billion for the Higher Education Commission (HEC) in the current budget. In addition, the HEC has been granted Rs44 billion for development programmes, which is 67 per cent more than the previous year.

Miftah Ismail said that this is a demonstration of our commitment to the youth. We are encouraging provinces to completely fulfill their obligations in terms of higher education promotion in the coming years, he said. The HEC budget includes 5,000 scholarships for Balochistan and tribal district students. He added that a unique scholarship programme has been introduced for Balochistan’s coastal communities.

The Finance Minister said that 100,000 laptops would be provided to students around the country on affordable instalments. Funds have also been set aside for the purchase of cutting-edge equipment to improve engineering and technology education.

15 per cent Increase in govt employees’ salaries

In Budget 2022-23, Miftah Ismail announced a 15 per cent increase in government employee salaries, as well as the merger of adhoc allowances.

He said that the tax on savings certificates, pensioners’ benefit accounts, and martyrs’ family assistance accounts had been reduced from 10 per cent to 5 per cent.

Small merchants will be subject to a new fixed income and sales tax regime, according to the Minister. Electricity bills would be used to collect taxes ranging from Rs3,000 to Rs10,000 under this method. This will be a final agreement, and FBR will have no right to inquire about the tax.

According to Miftah Ismail, a proposal has been made to increase initial depreciation rates for industries and other businesses from 50 per cent to 100 per cent in the first year.

Furthermore, he stated that any tariffs imposed on industrial units during the import of raw materials will be considered adjustable in order to protect the business community’s working capital.

New industrial policy

He stated that an industrial policy is being implemented in partnership with the Asian Development Bank in order to boost the country’s industrial base. He stated that the Prime Minister has directed that all exporter claims be resolved as soon as possible.

A sum of Rs40.5 billion is due to them right now, and we will pay it as soon as possible. Regardless of financial challenges, sales tax refunds are issued swiftly. Industrial feeders have been spared from load-shedding, according to him, in order to ensure that the industrial sector has uninterrupted power supply.

A new strategy for promoting investment in the country is being developed which aims to provide an enabling atmosphere for investors by eliminating the lengthy procedure. The government will overhaul the dispute settlement structure to make it easier for domestic and foreign investors.

Boosting agriculture sector

Talking about the agriculture sector, Finance Minister stated that Rs21 billion had been set aside to boost agriculture and livestock productivity. He stated that the Ministry of Food Security, in consultation with the Planning Commission and the provinces, has developed a three-year growth strategy. This plan aims to increase agri-production, increase farmer prosperity, and promote smart agriculture and self-sufficiency.

National Youth Commission

The Finance Minister also announced the development of a National Youth Commission to help youth realise their full potential. Various plans for the youth, he noted, have been offered. He stated that a coordinated strategy is being implemented to strengthen the role of educated youth in the growth of the country. According to him, the youth employment initiative will create over two million job chances.

He added that a scheme to foster youth entrepreneurship will be launched, under which interest-free loans of up to Rs500,000 and loans of up to Rs25 million will be made available on easy payments. He stated that in this lending arrangement, a 25 per cent quota has been been aside for women. He stated that women will be given precedence in hi-tech training in order to achieve economic empowerment. Youth development centres would be set up over the country, he said.

A green youth movement would be launched to involve young people in environmental initiatives. Funds will be set aside to distribute laptops on a merit-based and instalment basis, as well as the construction of 250 mini-sports stadiums across the country. Miftah Ismail stated that an innovation league would be established in order to improve the youth’s potential. He said that a talent quest and sports drive programme will be developed for youngsters between the ages of eleven and twenty-five.

Reduction in govt spending

According to the Finance Minister, the current government’s top focus is austerity. This budget includes a reduction in government spending, and we are taking meaningful moves in that direction. He stated that automobile purchases will be completely prohibited. Apart from development initiatives, procurement of furniture and other products would be prohibited. Cabinet members and government officials will have their gasoline quotas lowered by 40 per cent. There will also be a ban on international tours paid for by the government, with the exception of the most important ones.

A medium-term macroeconomic framework has been established to put the economy on a road of development, according to the Finance Minister. He emphasised his belief that by implementing this framework, we will be able to steer the economy in the right way. Our biggest problem, he remarked, is to expand without a current account deficit. As a result, a minimum of 5 per cent will be obtained without disrupting the balance.

Improved fiscal and monetary policy

He said that the GDP will increase from Rs67 trillion to Rs78.3 trillion in the coming fiscal year and the government is attempting to lower inflation through improved fiscal and monetary policy. During the next fiscal year, inflation will be decreased by 11.5 per cent.

He predicted that the tax-to-GDP ratio will rise to 9.2 per cent in the coming fiscal year, up from 8.6 per cent now. He noted that in 2017-18, we had kept this ratio at 11.1 per cent. He stated that the overall deficit, which is currently at 8.6 per cent, will be steadily reduced. In the coming fiscal year, this will be reduced to 4.9 per cent. Similarly, the overall primary balance, which presently stands at -2.4 per cent of GDP, will be reduced to 0.19 per cent.

Import and export

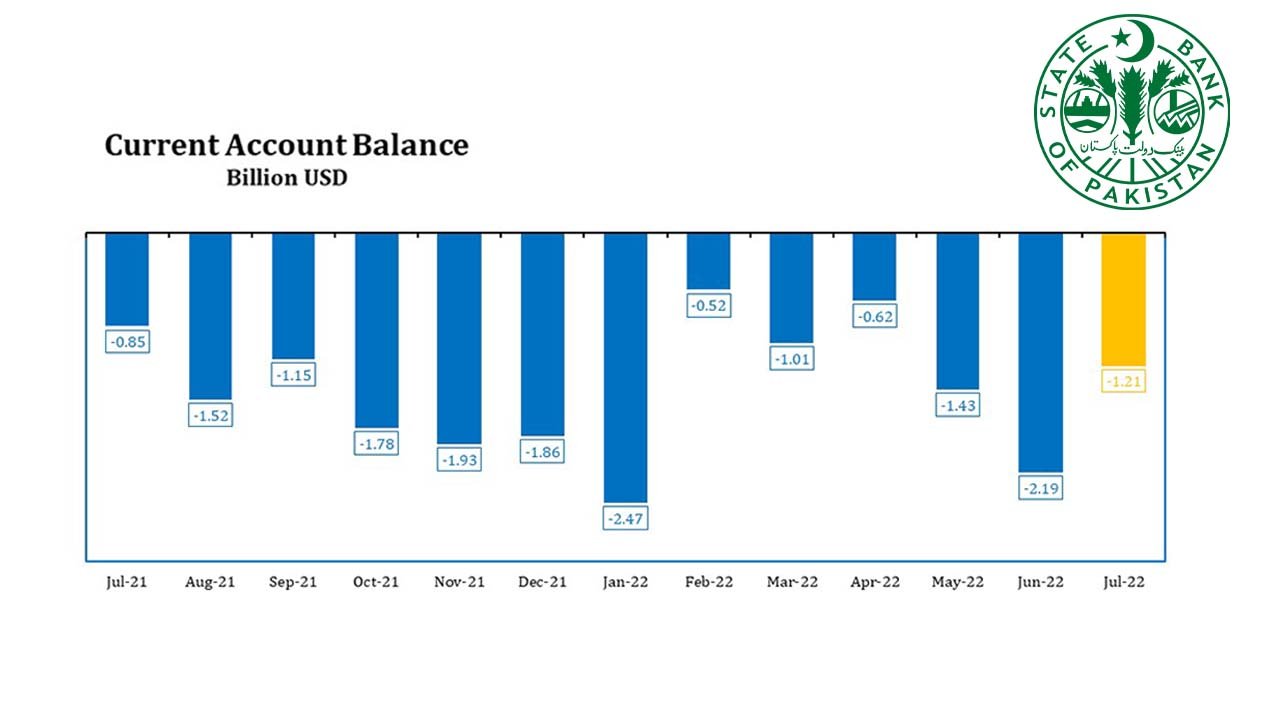

Imports, which are estimated to be $76 billion this fiscal year, would be lowered to $70 billion the following fiscal year, according to the Finance Minister. Exports are currently $31.3 billion, but will increase to $35 billion in the coming fiscal year. The current account deficit will be decreased from -4.1 per cent of GDP to -2.2 per cent of GDP.

Remittances, which are predicted to continue at $31.1 billion this fiscal year, are expected to grow to $33.2 billion next fiscal year.

Key allocations in Budget 2022-23

Rs1,523 billion allocated for defence

Rs800 billion allocated for Public Sector Development Program (PSDP)

Rs699 billion allocated for targeted subsidy

Rs364 billion allocated for Benazir Income Support Program (BISP)

Rs64 billion allocated for Higher Education Program

Rs25.99 billion allocated for Atomic Energy Commission

Rs24 billion allocated for Health

Rs21 billion allocated for Benazir Nashunuma Program

Rs11 billion allocated for Agriculture

Rs10.12 allocated billion for food security

Rs9.60 billion allocated for Climate Change

Rs530 billion allocated for pension funds

Rs3.46 billion allocated for Maritime Affairs

Key announcements

The GDP growth target has been set at 5 per cent.

Remittances are expected to total $33.2 billion.

Inflation will be held at 11.5 per cent.

FBR has set a revenue target of Rs7,004 billion.

Non-tax revenue objective is set at $2 billion.

The goal set for imports is $70 billion.

The target for exports is $35 billion.

Government employees will have a 15 per cent raise in pay.

Under a new employment scheme, youngsters will be eligible for interest-free loans up to Rs500,000.

Distributors and manufacturers will no longer be subject to an 8 per cent withholding tax.

On national saving systems, the profit rate dropped from 10 per cent to 5 per cent.

Cinema owners and film makers are exempt from income tax.

On cars with engines larger than 1600cc, the advance tax will be raised.

Pharmaceutical materials are exempted from any customs duties.

This is a developing story..