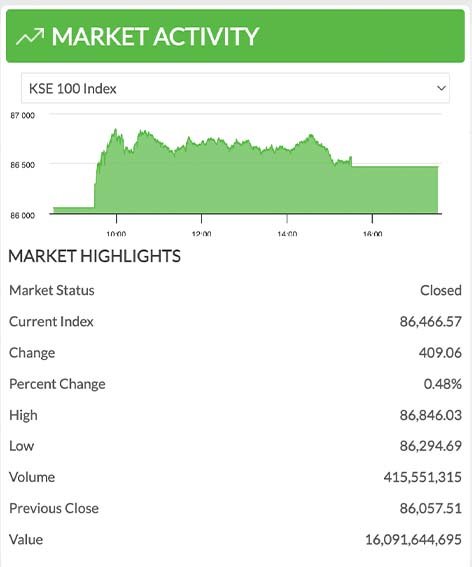

Pakistan Stock Exchange (PSX) opened Tuesday on a positive note and managed stay nearly 600 points up throughout the trading session.

The benchmark KSE-100 index was seen at its highest level during the day session when it surged to record peak of 86,846.03 points at 9:59 AM after rising by 788 points from its last close of 86,057. This occurred when the volume stood at 36,842,210.

Interestingly, the lowest point PSX witnessed was also recorded at the opening hour, around 9:30 AM, when the stock market was seen at its lowest point for day, reaching 86,294.69.

Still, throughout the day, the KSE-100 index managed to stay in in the positive territory and ended the second trading session of the week in green with a new record high of 86,466.57.

The total volume of the KSE-100 index was 415.551 million shares.

The PSX closed with a gain of 409 points or 0.48 per cent.

| Market summary | Details |

| Overall performance | 63 companies closed up, 34 closed down, 3 were unchanged. |

| Top gainers | KEL (+13.41%), ATRL (+8.28%), SYS (+7.44%), CHCC (+6.03%), MEHT (+5.19%) |

| Top decliners | PAKT (-6.18%), PGLC (-5.41%), PIBTL (-4.40%), EPCL (-2.95%), YOUW (-2.42%) |

| Index-point contributors (Up) | SYS (+174.04 points), LUCK (+62.46 points), HUBC (+51.71 points), ATRL (+48.33 points), KEL (+44.48 points) |

| Index-point contributors (Down) | FFC (-108.64 points), PAKT (-29.07 points), PSO (-21.78 points), BAHL (-20.80 points), EFERT (-17.23 points) |